Why UK Banks Block Gambling Payments and How Withdrawals Work

Loading...

A lot of people first run into the workings of bank gambling blocks at the worst possible moment: when a deposit fails, or when a withdrawal they were promised does not arrive. The mechanics are not complicated once you see them laid out, and understanding them is the difference between knowing why a payment stalled and assuming the casino simply stole your money. This page is about the plumbing, not about getting around it.

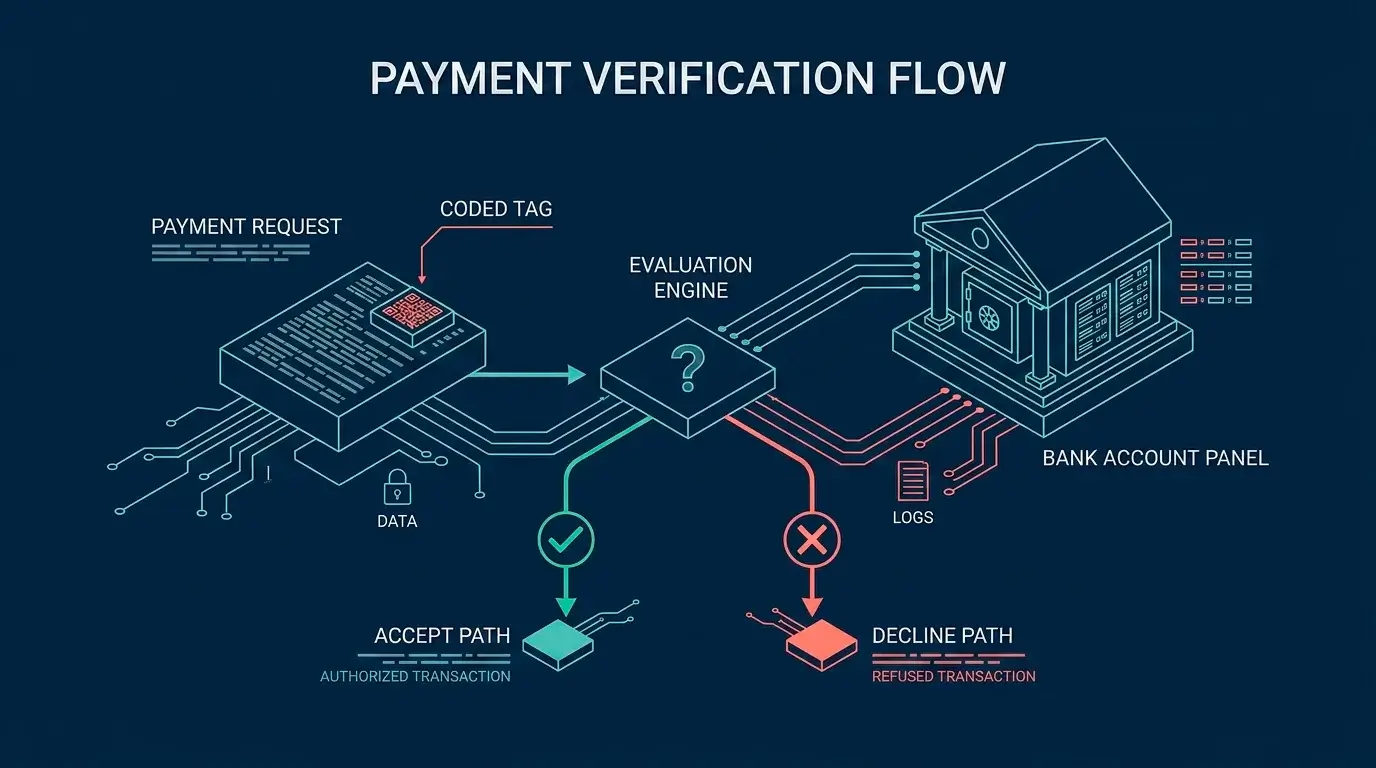

How the block actually fires: merchant category codes

Every business that takes card payments is tagged with a merchant category code, a four-digit number assigned by the card networks that tells banks what kind of transaction is taking place. Gambling sits primarily under code 7995, labelled for betting, with related codes such as 7800, 7801 and 7802 also used for lotteries and similar activities.

When your bank sees a payment request coded 7995, it can check that against your account settings and decline it before any money moves. That timing matters: the block is a gate at the front, not a refund after the fact. If you have a gambling block switched on, or your bank declines the category by default, the transaction never completes in the first place.

This is also why the experience can feel inconsistent. Two casinos can both be gambling sites, yet one payment goes through and the other is declined, purely because of how each operator’s payment processor has coded the transaction.

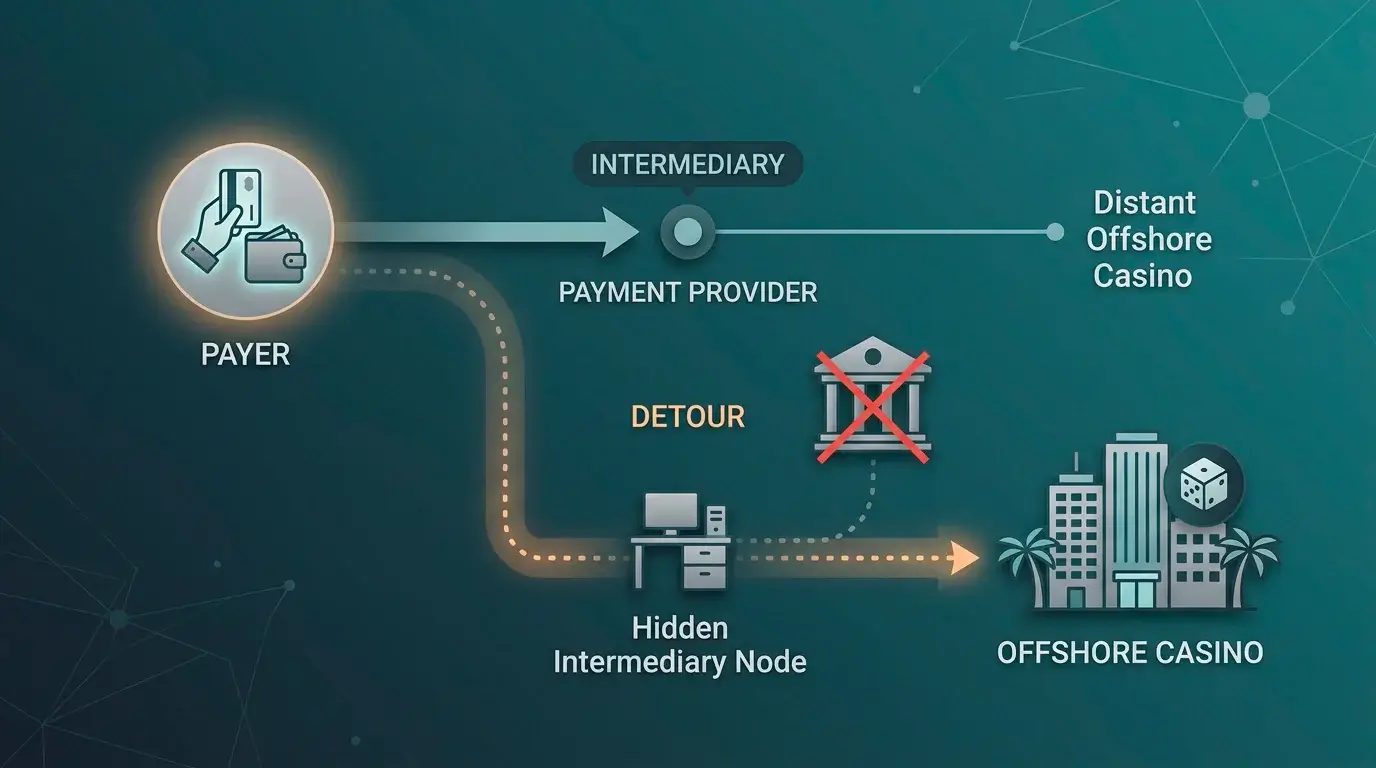

Why some offshore payments slip through anyway

The category-code system has a clear limitation: it only works if the transaction is actually coded as gambling. If an operator routes a deposit through a third party, or uses a payment processor that codes the charge under a non-standard category, the bank never sees a 7995 tag and the block does not fire. This is precisely how some offshore casinos manage to accept deposits that a player’s bank would otherwise refuse.

It is worth being clear about what that means rather than how to do it. A payment that slips past your bank’s gambling block has bypassed a protection you may have deliberately turned on. That is the opposite of reassuring. If the appeal of an offshore site is that your bank cannot see what the money is for, that is a signal worth sitting with, and it connects directly to the wider picture of safety risks at offshore sites. The same opacity that lets a deposit through also makes a dispute much harder later.

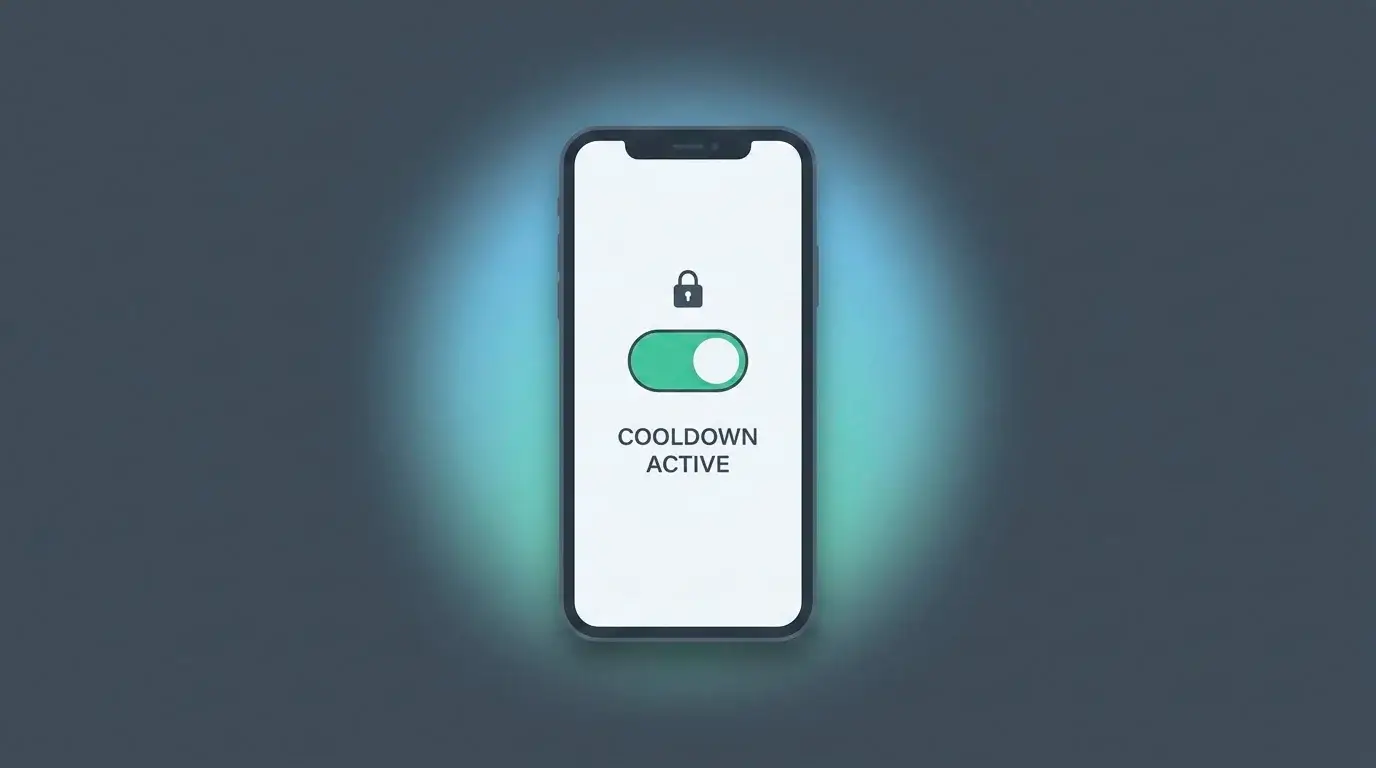

The gambling-block tools your bank already offers

Most major UK banks now offer a gambling-transaction toggle inside their app. Switch it on and the bank declines transactions coded as gambling, often with a built-in delay before you can switch it off again, so a late-night impulse cannot be reversed in the same moment. These tools are free, and they are one of the more effective low-friction protections available.

The honest framing is that these toggles are a consumer-protection feature, not an obstacle. A casino designed to defeat them is not solving a problem for you; it is removing a brake you chose to apply.

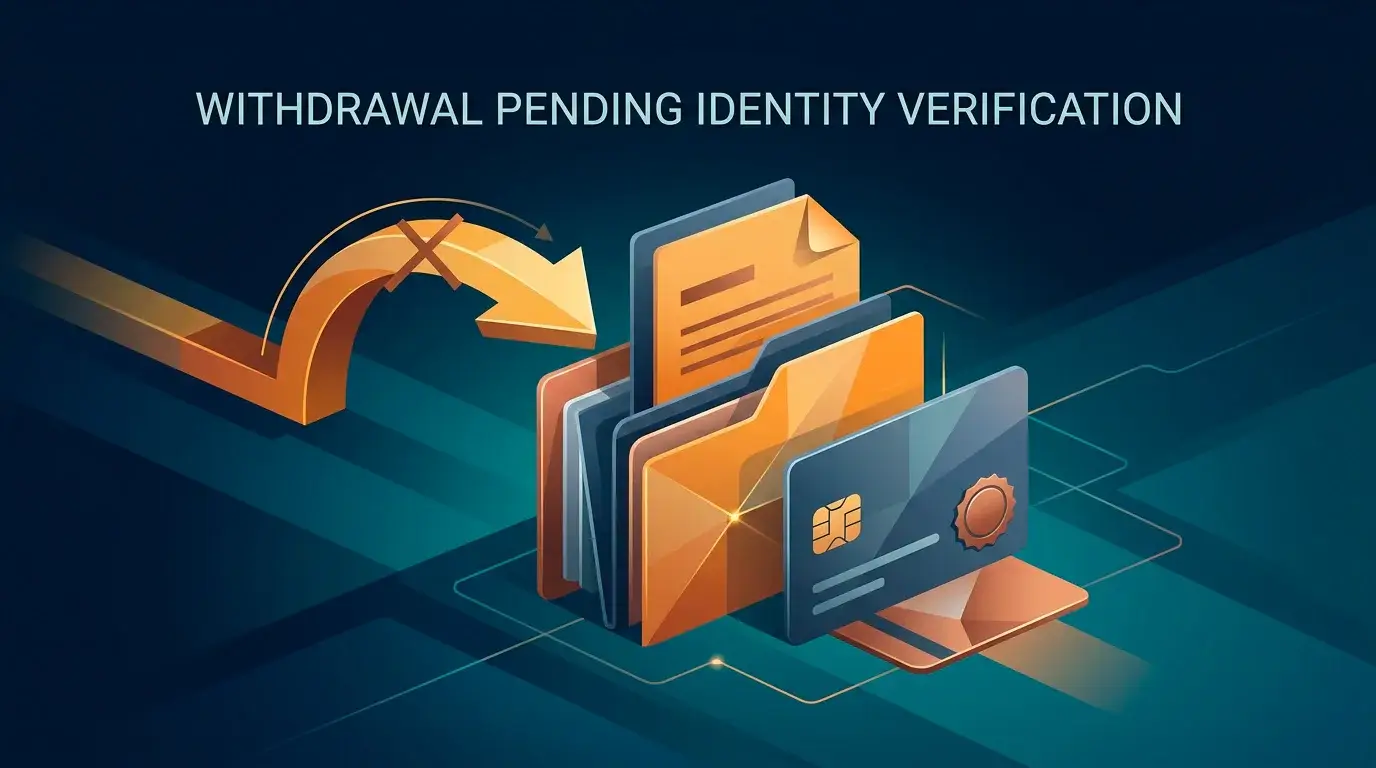

Getting money out: the KYC flip at withdrawal

Deposits and withdrawals are not symmetrical, and offshore sites exploit that gap. A casino can advertise a smooth, no-questions-asked deposit and then demand a full set of identity documents the moment you try to cash out. A site that felt like a no-KYC experience on the way in can flip to aggressive ID checks on the way out, and a withdrawal can sit frozen while documents are reviewed, re-requested or rejected.

That is not always fraud; KYC checks are a legitimate part of anti-money-laundering compliance. But the timing – relaxed at deposit, strict at withdrawal – is also a documented pattern in genuine withdrawal traps, where the checks become an excuse for a payout that never arrives. The two situations can look identical from the player’s side, which is exactly why the pattern is worth knowing before you deposit. Our page on withdrawal traps and scam flags goes into the deliberate version in detail.

On top of the casino’s own checks, your bank has to be willing to accept the incoming payment. An offshore payout routed through an unfamiliar processor can itself trigger a fraud review on the receiving side, adding another layer of delay that has nothing to do with the casino.

Why chargebacks rarely rescue a gambling loss

People often assume a card chargeback is a safety net. For gambling, it largely is not. Visa and Mastercard treat a gambling deposit coded 7995 as payment for a service that has been delivered – the chance to play – the moment the deposit lands. Because the service is considered provided, the usual grounds for a chargeback are sharply limited, and disputes over gambling losses are routinely rejected.

This is a meaningful gap. With a regulated UK operator there are formal complaint and escalation routes; with an offshore site there is no UK Gambling Commission to appeal to, and the card-network chargeback you might fall back on is mostly closed off by how the transaction is classified. To understand how thin the offshore protection layer really is, it helps to read this alongside casinos not on GamStop explained, which sets out what the workaround does and does not give you.

- Deposit coded 7995

- Treated as a delivered service, so chargeback grounds are limited from the outset.

- No UKGC oversight

- No regulator-backed complaints route if an offshore operator withholds funds.

- Crypto deposits

- No chargeback mechanism exists at all once the transaction confirms.

The credit-card ban in the background

One regulatory fact sits underneath all of this. Since 14 April 2020, UK-licensed operators have been prohibited from accepting credit cards for gambling, under a licence condition the Gambling Commission introduced after finding that a high share of credit-card gamblers were at risk of harm. The ban applies to online and offline gambling alike, with only face-to-face lottery purchases excepted.

That ban is one reason offshore sites stand out: many will still take a UK credit card precisely because they sit outside the UKGC rulebook. You can read the regulator’s position on the UK Gambling Commission site, and the government’s wider gambling-policy material on GOV.UK. The point for this page is simple: a credit-card deposit that your bank or a UK casino would refuse can still go through offshore, and a credit-card charge carries its own debt risk on top of everything else above.

What this means before you move money

Read together, these mechanics describe a system where the protections that exist at the UK-regulated edge – the block, the chargeback, the regulator – thin out or disappear the further offshore you go. None of this is a how-to for defeating a bank’s block, and it should not be read as one. It is a map of where the consumer protections sit so you can see clearly what you give up by routing around them. For the deposit side of the same picture, see the payment methods offshore sites accept.

This material was created by the Unlicensed Casino Zone team.

Related posts

Spotting Risks and Scam Red Flags at Non-GamStop Casinos

Curaçao, Anjouan and Malta Licences Compared for UK Players